Due to the fact that every business transaction involves the exchange of money, finance is believed to be engaged in every aspect of a company’s operations. It’s obvious that it’s overly broad. The group of individuals defines scope of strategic financial management as the acquisition of funds and the successful application of those funds within a company, despite the fact that money can be acquired and applied in other organizations. Because of this, the firm’s scope of strategic financial management must guarantee that higher earnings are adequate to cover the costs and risks associated with initiating and running the project.

As a result, from the perspective of a corporate unit, nature of strategic financial management is not only about ‘fundraising,’ but it is also about efficiently managing the company’s resources. It is not a difficulty in a mature capital market to raise funds; rather, the issue is employing capital resources efficiently through financial planning, organizational structure, and control systems.

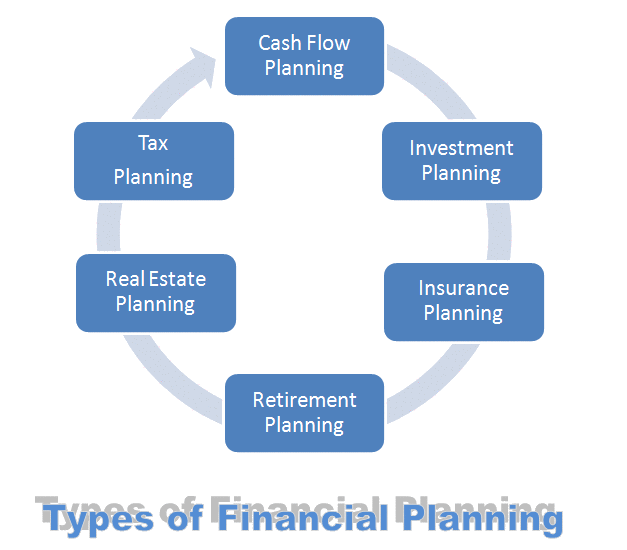

Scope of Strategic Financial Management

A major portion of the criteria for investment decisions is devoted to budgeting for and controlling capital expenditures through the application of analytical approaches. Payback period, accounting rate of return, and discounted cash flow techniques are all examples of financial concepts (net present value, etc.) We will go through each of these scope of strategic financial management in further detail which helps to facilitate decision-making.

Discounted BCR (Benefit-to-Cost Ratio)

The reliability of this ratio is enhanced because it is based on the present worth of future benefits and costs. Alternatively, it can be expressed as gross or net, as in the preceding scope of financial management example. It takes into account all revenues, regardless of when they are received, and as a result, it is consistent with the “larger and better” notion.

A discount component has been added to early receipts, which means that early receipts are given more weight than late receipts. This ratio satisfies the requirements of both principles and serves as an appropriate criterion for decision-making.

Non-Discounted BCR (Benefit-to-Cost Ratio)

It is defined as the relationship between the total benefits and the whole expense of the project. Benefits are paid out at their face value. The ratio may be expressed as “gross” or “net.” It is referred to as “gross” when it is estimated with benefits and without deducting depreciation. Before computing results in the net version, depreciation is deducted from benefits in order to compute the outcomes. Both ratios result in the same ranking position.

The net ratio is the same as the gross ratio minus one. Because of this link, it is simple to compute gross ratio and, as a result, arrive at the net ratio. It is OK to use this criterion in scope of strategic financial management with the “larger and better” notion. However, it does not adhere to the second idea of “bird in hand” because early earnings are given the same weight as later collections throughout the project’s lifespan.

Present Value (PV) / Net Present Value (NPV)

This concept is essential as a selection criterion because it draws attention to the fact that the value of money is always decreasing, as a rupee acquired today is worth more than a rupee received at the end of a year. As a scope of strategic financial management result, a rupee received at the end of a period of n years is worth 1/(1+i)n dollars today. Investment decisions entail a comparison of the present value of assets with the cost of assets; if the present value exceeds the cost, the investment is deemed acceptable.

Another off-shoot of this criteria is the net present value method, which is closely related to the cost-benefit ratio in terms of its application. It takes into account all of the revenue as well as the amount of time spent with appropriate weights. Rather of evaluating the ratio in a cost-benefit analysis, the difference in current value of benefits and expenses is assessed here.

This criterion is critical for approving projects that have a positive net present value at the company’s cost of capital rate, which is the case in most cases. It may be used to decide between two projects that are mutually incompatible by determining if more expenditure will result in a positive net present value in the future.

Make Renovation / Restoration

The payback selection criterion does not adhere to the ideas outlined above, namely “the larger and better” and “the bird in hand.” It completely disregards the first principle since it does not take into consideration the cash flows that will be generated once the investment has been recovered. It also does not fully comply with the second principle, because it assigns no value to the receipts once the money has been recovered, therefore violating it.

When picking this criterion for investment selection, it is critical to consider the amount of time available. The selection is made on the basis of the investment’s ability to pay off its debt as quickly as possible. Pay back is a simple term that refers to the time it takes for cash flows from a project to be used to reimburse the initial investment to the firm’s account. It is decided which projects will be selected on the basis of this criterion since they would have faster payback times.

Return on investment (ROI)

It provides an extra choice criterion for scope of strategic financial management based on accounting records or expected financial statements to measure profitability as a yearly proportion of total capital employed (annual percentage of capital employed). The rate of return is achieved by employing two separate techniques for processing revenue in the analysis, each of which yields a different set of conclusions.

After deducting the depreciation charge, the average revenue generated by the investment is taken into consideration in the first scenario. Rather than using the average investment as the denominator in the second case, it is the starting cost that is used.

This provides the fundamental annual rate of return. This is founded on the idea of “larger and better.” This criterion can be applied either to the average investment in the year chosen for research or simply to the beginning cost of the research project itself.

Internal Rate of Return (also known as IRR)

It is a criterion that is frequently used while making investment decisions. IRR is referred to as marginal efficiency of capital or the rate of return above the cost of capital. In addition to nature of financial management, it specifies a rate of discount that will be used to balance the present value of net benefits with the cost of the project. This method satisfies both of these requirements.

The variables taken into consideration while making finance decisions, with particular reference to the capital structure of a business unit, can be discussed in detail below. When analyzing a corporate unit’s capital structure, it is important to note that it has two key characteristics: ownership capital (also known as equity) and debt, which represents the interest of debenture holders in the firm’s assets.

Tax savings, ease of sale, lower cost of flotation and services, lower cost of capital, the advantage of leverage, no dilution of equity and probable loss of control, the logical consolidation and funding of short-term indebtedness through a bond issue, the inflationary trend of rising interest rates, and the improvement in financial ratios are the factors that contribute to the inclusion of debt in a company’s capital structure.

Urgency of a Project

For investment projects in various corporate units, commercial businesses, and government organizations, the use of the word “urgency” is regarded a factor in the selection process. Under scope of strategic financial management, the following criteria are used to determine the urgency of a project:

- Provides enough justification for undertaking the project;

- It maximizes profits;

- It contributes immediately to the achievement of the project’s objectives.

Despite the fact that urgency as a criterion lacks objectivity due to the fact that it is not quantifiable, it clearly provides an ordinal rating scale for the selection of projects on a preferred per-exemption basis, which is useful for project selection.

Conclusion

When a company needs money, it has little choice but to seek equity financing to meet its financial obligations. Only on the basis of a sufficiently strong equity foundation can a company obtain debt, which serves as a cushion against future debt financing. For the purpose of determining the best combination of debt and equity financing sources, the scope of strategic financial management examination the effect of leverage is a key focus. As a result, it is desirable to investigate this criterion for financing decision-making in terms of leverage and cost of capital in more detail.