The accounting process, to some extent, is also known as the accounting cycle. Today’s accounting software has transformed traditional accounting methods. But still process of accounting and accounting cycle remains the same irrespective of traditional or modern accounting methods. In this topic we will initially understand what is accounting cycle followed by the three steps in the accounting process, process of accounting with examples and then seven steps of accounting cycle in depth.

The ability to comprehend financial figures is critical for business owners. They are essential for tasks like as budgeting money, selling your firm and acquiring funding which would be impossible without them. The business must execute these procedures continuously, enabling it to generate new and current financial statements regularly, as the term suggests.

What is Accounting Cycle?

The Accounting Cycle comprises a series of accounting activities aimed at generating financial statements by categorizing, recording, and summarizing accounting information. Completing the accounting cycle involves conducting the entire sequence of accounting activities in the correct order within a single accounting period. It is also refer to as the bookkeeping cycle or the accounting process.

The accounting process initiates when a transaction occurs, beginning with recording the transaction into the books and extending until it manifests in the financial statements by the end of the accounting period.

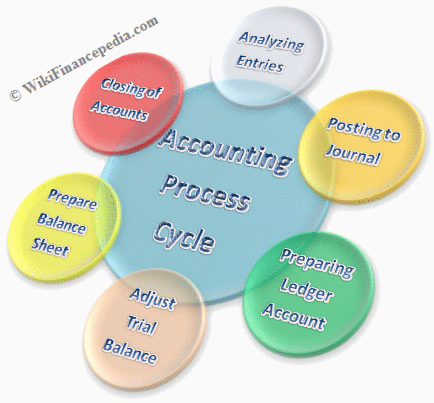

Throughout the year, the accounting cycle transforms all raw financial information of your company into financial statements through a seven-step process. Later in this article, we will delve deeper into these 7 steps of the accounting cycle.

Key 3 Steps in the Accounting Process

The accounting process involves recording company activities in accounting records through three distinct types of transactions: accrual accounting, accrual accounting, and accrual accounting. Accrual accounting records company activities in the accounting records.

The organization integrates various types of information to generate financial statements. The following are the three steps in the accounting process to sorts the transactions.

- Firstly, complete and document the first transaction type to ensure that reversing entries from the previous period have indeed been reversed.

- Next, adhere to specific procedures to record corporate transactions in accounting records, known as second-tier processes.

- Lastly, perform period-end processing to close the books and prepare financial statements for the period under consideration.

Important 7 Steps of Accounting Cycle

Here we will provide the detail explanation on key important 7 steps of accounting cycle which is an elaborate following the 3 steps in the accounting process so that you can understand accounting in much more better ways.

Analyze and categorize Transactions

The first step in the accounting process involves analyzing and categorizing transactions before posting them into books of account. At first, categorize transactions as either business or personal. Only business transactions will then be entered into the accounting system. Let us understand process of accounting with examples for reference here. For example: When journal entry says, Mr. Patel taken a personal loan of Rs.4,50,000/- from Citibank. While analyzing, categorize it as a personal entry and exclude it from business accounting considerations.

Posting transactions into Journals

The double entry system, regardless of whether it is manually maintained or computerized, records all business transactions. Each transaction credits one account and debits another in a journal entry.

Frequently occurring transactions are documented in specialized journal books like the sales journal, cash receipts journal, and purchases journal. In contrast, less frequently encountered transactions are logged in the general journal book.

Preparing Ledger Accounts

In the accounting process, ledger accounts serve as the final book of entry. After recording all transactions in the ledger account, one can determine ledger balances. For example: When posting all the bank related debit and credit journal entries into Bank’s ledger account, Once can figure out increase or decrease in bank A/c. This can assist business to take precautionary steps in case of deficit for next year.

Preparing Trial Balance

Main purpose of maintaining trail balance is to match debit and credit balances extracted from ledger accounts. Total of all the debit amount of trial balance should match with credit amount of trial balance.

If the trial balance fails to match, it is necessary to take immediate action. We should conduct re-engineering to identify errors and omissions. Additionally, we must implement proactive measures within the accounting process to rectify these errors.

Adjustments in Trial Balance

Sometimes, businesses incur expenses but mistakenly fail to record them in journals. Preparers make adjusting entries before compiling financial statements when they overlook certain incomes during journal posting, leading to a mismatch between credit and debit trial balances. This ensures accuracy in financial reporting. These adjustments constitute the adjusted trial balance in the accounting process. Ultimately, at the end of all adjustments, the debit and credit balances of trial balances must be equal.

Preparing Financial Statement

After updating trial balance, it’s time to get close to the end stage in steps of accounting cycle. This process involves preparing financial statements for an individual, business, or organization for the accounting year. During this process, the following reports are prepared:

- Income statement or Profit / Loss statement.

- Change of Equity statement.

- Balance sheet or financial position statement.

- Cash Flow statement.

- Annotations to financial statements.

Closing Entries

This is the final stage in steps of accounting cycle. In this process, we close nominal or temporary accounts and carry forward balances to the next accounting cycle. We close accounts such as expenses, cash, income, and bank accounts. However, the balance sheet keeps permanent accounts open and does not close them.

Conclusion

Accounting cycle is a step-by-step technique for documenting company acts and events in order to keep financial records up-to-date. The length of a period in the conduct of a business is defined as one operational cycle, which might be one month, one quarter, or even one year in length. Hope you have very well understood the 7 steps of accounting cycle and three steps in the accounting process. Each accounting period will be covered by this technique, which will then be repeated the next period after that, and so on.

Read E-Learning Tutorial Courses - 100% Free for All

Basics of Accounting for Beginners

- Chapter 1: What is Accounting with Examples

- Chapter 2: Objectives of Accounting

- Chapter 3: Types of Accounts

- Chapter 4: Branches of Accounting

- Currently Reading: Accounting Process

- Chapter 6: What is Assets and Current Assets?

- Chapter 7: What is Liability and Current Liabilities?

- Chapter 8: What is Revenue and Expenses?

- Chapter 9: What is a Single Entry System?

- Chapter 10: What is Double Entry System?

- Chapter 11: What are Journal Entries? Format and Examples

- Chapter 12: What Is a General Ledger? Format with Example

- Chapter 13: What is a Trial Balance? Examples and Limitations

- Chapter 14: What is a Profit and Loss Statement or Income Statement?

- Chapter 15: What is a Balance Sheet? Definition, Format and Examples

- Chapter 16: What is Managerial Accounting? Role, Job and Objectives

- Chapter 17: Accounting Quiz – Basics of Accounting for Beginners Module