To show that total debits and total credits are equal, the trial balance is simply a list of all general ledger accounts and their balances. Accountants can ascertain each account’s balance by compiling this exhaustive list, which offers important insights into the entity’s performance and financial health.

The trial balance is more than just a set of figures, though. The foundation for the creation of financial statements is established in this initial stage of the financial reporting process. With the trial balance’s methodical arrangement of accounts and balances, accountants can spot mistakes and inconsistencies, fix them, and guarantee the accuracy of financial data.

Trial Balance Definition

In Accounting, Trial balance is a consolidated list of all the general ledger accounts of the business. Ledger accounts with debit balances appear in the debit column of the trial balance. Those with credit balances are listed in the credit column. This report utilizes the data to prepare both the profit and loss statements and the balance sheet of the business. Credit and debit trial balance should match. In-case of mismatch one has to rectify errors in nominal ledger accounts.

Today’s computerized accounting systems eliminate any clerical errors or omissions through accounting software. Consequently, the preparation of a trial balance is deemed less crucial in modern times. The assumption is that debit and credit columns will be equal, with any errors automatically rectified by the accounting software.

However in today’s world, trial balances are used by many companies for accounting and auditing purposes. Organizations who wish to disclose ledger balances prior to adjustments or ledger balances after proposed adjustments either publicly or for internally purposes maintain such statements.

Limitations of Trial Balance

Primary objective of trial balance accounting is to match debit and credit balances. This does not mean trial balance statement is error free. Below errors may still appear in it. Let us look into the limitations of trial balance further in this topic.

Error in Recording Transaction

The system will fail to detect the error if you enter an incorrect amount on both the debit and credit sides of a journal entry. For instance, mistakenly recording the purchase of machinery for Rs.40,000/- as Rs.4,000/- will go unnoticed.

Error of Omission

It will not be able to find error in-case if any of the transaction is missing. Excluding any transaction will still leave credit and debit balance as in-balanced.

Error of Principle

Suppose, correct amount added to accurate side (debit / credit) of the account but posted to account with different type. In such scenario, there won’t be any affect on totals of trial balance. For example, someone mistakenly debits travel expenses (expense account) to the stock account (asset account).

Error of Commission

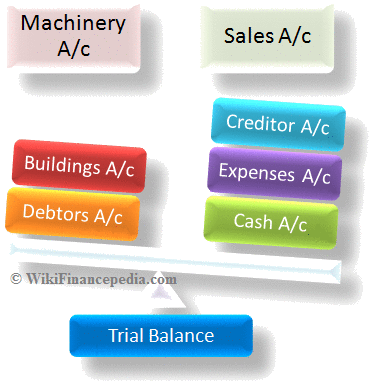

Posting a transaction to the wrong account of the same type does not affect debit and credit balances. For example, If someone mistakenly credits Machinery A/c instead of Buildings and Assets A/c, the balances will remain unchanged.

Error of Reversal

Incorrect application of any of the golden rules of posting entries leads to issues. Under such circumstances balances will still be in-balance. For example: If the correct entry is Machinery A/c debit to Account Payable A/c credit instead of Account Payable A/c debit to Machinery A/c credit still balances of both the sides will remain same.

Example of Trial Balance Accounting

| Xyz India Pvt. Ltd. | ||

| Trial Balances as of current assessment year. | ||

| List of Ledger Accounts | Debit | Credit |

| -Rs- | -Rs- | |

| Share Equity Capital A/c | 25,000 | |

| Machinery A/c | 35,000 | |

| Furniture & Fixture A/c | 10,000 | |

| Land and Buildings A/c | 75,000 | |

| Creditor A/c | 90,000 | |

| Debtors A/c | 4,000 | |

| Cash A/c | 1,000 | |

| Sales A/c | 20,000 | |

| Cost of good sales A/c | 7,000 | |

| General & Administration Expense A/c | 3,000 | |

| Total | 1,35,000 | 1,35,000 |

Conclusion

In addition, the trial balance is a crucial instrument for internal control, aiding in the identification of anomalies and fraudulent activity. By comparing debit and credit totals, accountants can spot discrepancies, protecting the accuracy of financial data and fostering greater openness within the company.

The trial balance represents the core of accuracy, reliability, and accountability in accounting procedures; it is more than simply a list of numbers. The Statement of Financial Position holds immense importance in financial reporting. It plays a pivotal role in establishing the foundation for accounting principles and practices. Its significance cannot be overstated.

Read E-Learning Tutorial Courses - 100% Free for All

Basics of Accounting for Beginners

- Chapter 1: What is Accounting with Examples

- Chapter 2: Objectives of Accounting

- Chapter 3: Types of Accounts

- Chapter 4: Branches of Accounting

- Chapter 5: Accounting Process

- Chapter 6: What is Assets and Current Assets?

- Chapter 7: What is Liability and Current Liabilities?

- Chapter 8: What is Revenue and Expenses?

- Chapter 9: What is a Single Entry System?

- Chapter 10: What is Double Entry System?

- Chapter 11: What are Journal Entries? Format and Examples

- Chapter 12: What Is a General Ledger? Format with Example

- Currently Reading: What is a Trial Balance? Examples and Limitations

- Chapter 14: What is a Profit and Loss Statement or Income Statement?

- Chapter 15: What is a Balance Sheet? Definition, Format and Examples

- Chapter 16: What is Managerial Accounting? Role, Job and Objectives

- Chapter 17: Accounting Quiz – Basics of Accounting for Beginners Module