Cash Conversion Cycle Definition:

Whenever a company invests its resources for a project, it expects profit out of it and the process takes time. The measure of time required by a company to convert its resource inputs into cash flow is measured in terms of cash conversion cycle. CCC (cash conversion cycle) is a metric that expresses the length of time, in days generally. Before the final product starts generating cash through its sales, the cash conversion cycle determines the sum of time each net input rupee is engaged in the production and sales process. The basic purpose of this particular metric is to monitor the time, time required to – sell the catalog, collect receivables and time needed for a company to clear all its bills without incurring penalties.

The CCC is also referred to as the “cash cycle” or “cash conversion cycle.”

Process of Cash Conversion Cycle (CCC):

Normally, most of the inventories acquired by a company are credit based; it further results in accounts payable. It is also not rare for a company to sell the finished products on credit; this leads to accounts receivable. As you can see, cash-in-hand or cash is not the initial concern. Its presence is required during payment of accounts payable and collection the accounts receivable. You must be wondering when cash conversion cycle is used then. Well, the cash conversion cycle evaluates the time between the pay out of cash and the cash recovery. Once can’t observe CCC unswerving in cash flows; rather, the cycle refers to the time period when a firm disburses the capital and till it collects back its receivables.

Cash Conversion Cycle Formula / Calculation:

The formula for calculating CCC is as follows CCC = DIO + DSO – DPO.

Now let’s understand the term used for cash conversion cycle calculator.

- DIO – Number of days taken by a company to sell its inventory is known as Days Inventory Outstanding or simply abbreviated as DIO. Shorter the DIO, better sales for the company.

- DSO – Once the products are sold, days required to collect all the account receivables by a company is called as Days Sales Outstanding. Again, smaller DSO is preferred.

- DPO – Days Payable Outstanding refers to time a company takes to pay all its bills, accounts payable per se. Longer DPO is favored, for it enables the company to have cash in hand for more time, which increases its investment potential.

Calculation of CCC requires various items from financial statements for a particular period of time – the accounting time for one calendar year is 365 days and for one quarter it is 90 days.

Cash Conversion Cycle Example:

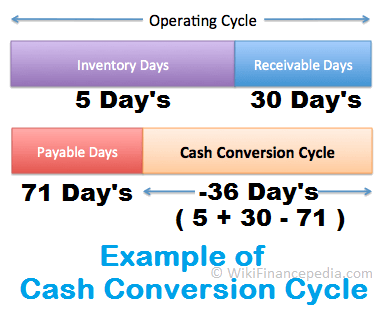

Jack Smith is a retailer that sells electrical and hardware equipment. Jack purchase it from one of the vendor and pays the amount within 10 days to get a handsome discount. Jack is on a high inventory turnover ratio and can collect accounts receivable from his customer within 30 days of period on average.

Jack’s CCC calculations is as follows:

DIO represents – Inventory Outstanding Days: 15 day’s

DSO represents – Sales Outstanding Days: 2 day’s

DPO represents – Payable Outstanding Days: 12 day’s

Jack’s cash cycle is calculated like this:

15 Day’s + 2 Day’s – 12 Day’s = 5 Day’s

Now you know, Jack’s cash conversion cycle is 5 days. This means Jack takes 5 days from paying for his inventory to receive the cash from its sale. Jacks would have to compare his cycle to other companies of his industry to see if his cycle needs to be improved or it’s reasonable.

Importance of Cash Conversion Cycle:

The efficiency of a company’s management and, therefore, the general health of a company are determined by cash conversion cycle. The result, based on the calculation using the above mentioned formula appraises the rate by which a company can convert cash on hand into inventory and accounts payable, in the course of sales and accounts receivable, and then back into cash. Once calculated, these activity ratios can be combined to indicate the effectiveness of management’s capability to utilize short-term assets and accountability to produce cash for the company.

The CCC involves the liquidity risk coupled with growth by computing the time during when the company will be short of cash or deprived of cash if it raises resource input investment in order to elevate its sales. Cash conversion cycle can be used as an effective tool to compare your company’s management amongst your competitors. To make it simpler, a low Cash Conversion Cycle implies that the company’s monetary assets are very well managed, this can further help in appraising potential investments. Along with the return on assets and return on equity, CCC can serve as an indicator of supervision efficacy and company viability.

The cash conversion cycle holds high value of significance for retailers and similar businesses, albeit is useful in every industry. The evaluation demonstrates the pace of conversion of products into cash through sales. Thus shorter the cycle is preferable. Because this signifies that capital tied in the business process is for short time span, and this is better for the company’s bottom line.

Read E-Learning Tutorial Courses - 100% Free for All